Then a depreciation amount per unit is calculated by dividing the cost of the asset minus its salvage value over the total expected units the asset will produce. Each period the depreciation per unit rate is multiplied by the actual units produced to calculate the depreciation expense. We’ve already fully depreciated this asset all the way to its residual value, okay? So there’s going to be no more depreciation even if we go into year 7, year 8.

Recording straight-line depreciation in your accounting system

So after 1 year, after we’ve depreciated it for 1 year, well our cost was $42,000 minus accumulated depreciation. Well, it’s only been 1 year, so we’ve only accumulated 1 year of depreciation which is $8,000 and our net book value is the $42,000 minus $8,000. So just to reiterate how we might see this on a balance sheet here, I’m trying to get out of the way so you can see behind me. So I’ll try and stay out of the way, and I’ll do it here on the side. So what we’ve got, we would show our assets just like we do on any balance sheet, right?

Straight-Line Depreciation for Tax Purposes

So, the company will record depreciation expense of $7,000 annually over the useful life of the equipment. The asset will accumulate 2.5 years of depreciation out of its total useful life of 5 years. We can simply multiply the annual depreciation amount by 2.5 to calculate the accumulated depreciation. Using this amount, we can calculate the depreciation expense, accumulated depreciation, and carrying value of the asset for each year as follows. In case you’re confused at any step, read the explanation below the depreciation schedule. All accounting years other than the first and the last one are charged depreciation expense in full using the straight line depreciation formula above.

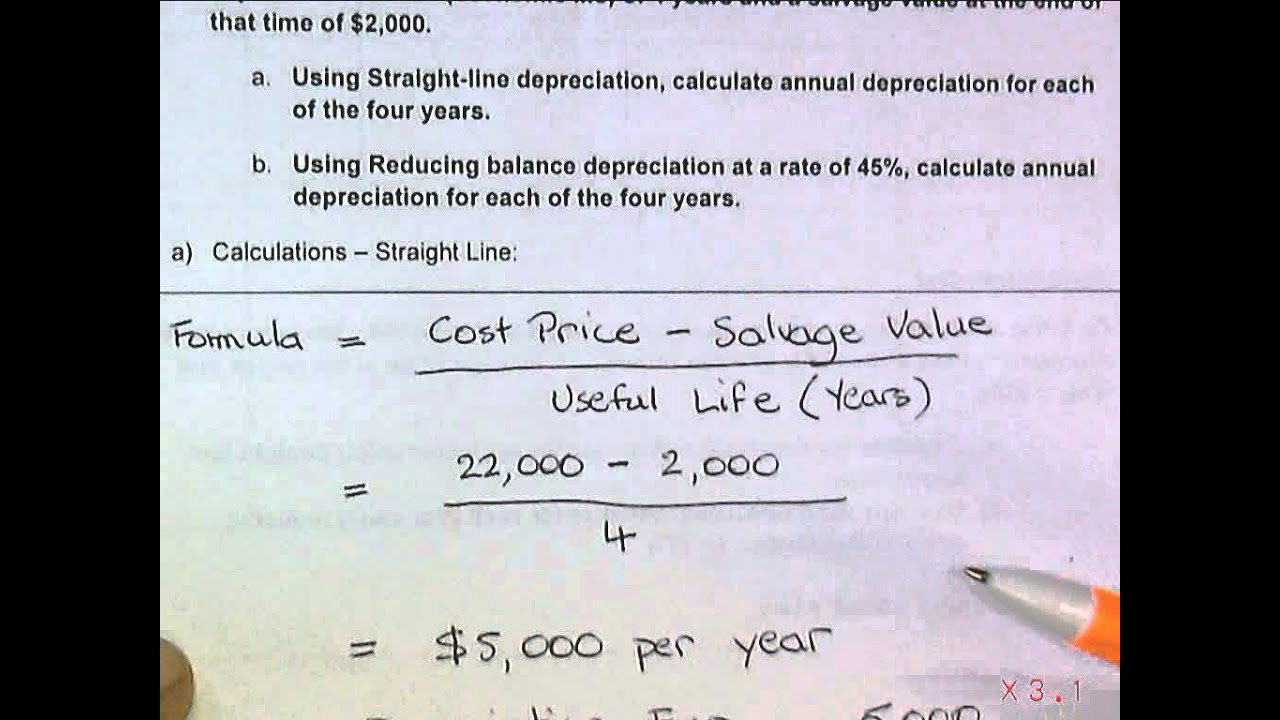

- In the explanation of how to calculate straight-line depreciation expense above, the formula was (cost – salvage value) / useful life.

- This method also adheres to the matching principle in GAAP, ensuring that expenses are matched with the revenues they help generate.

- It is used when there’s no pattern to how you use the asset over time.

- Depreciation expense represents the reduction in value of an asset over its useful life.

- Let’s assume that Company A buys a piece of equipment for $10,500.

Your Financial Accounting tutor

This makes them suitable for straight line depreciation by allocating the initial cost evenly over their estimated useful life. Tangible Assets are physical items that can be seen and handled. Common examples of tangible assets include machinery, equipment, and furniture and fixtures. These assets typically have a predetermined useful life, which makes them suitable for the straight line depreciation method.

What is the approximate value of your cash savings and other investments?

The calculation is done by deducting the salvage value from the cost of the asset divided by the number of years of useful life. While the purchase price of an asset is known, one must make assumptions regarding the salvage value and useful life. These numbers can be arrived at in several ways, but getting them wrong could be costly. Also, a straight-line basis assumes that an asset’s value declines at a steady and unchanging rate.

Next, you’ll estimate the cost of the salvage value by considering how much the product will be worth at the end of its useful life span. Dummies has always stood for taking on complex concepts and making them easy to understand. Dummies helps everyone be more knowledgeable and confident in applying what they know.

Here’s how to calculate gross, operating, and net profit margins and what they can tell you about your business. If you had to liquidate your business today, how much could you get out of it? According to straight-line depreciation, your MacBook will depreciate $300 every year. Our intuitive software automates the busywork with powerful tools and features designed to help you simplify your financial management and make informed business decisions.

In the United States, residential rental properties are depreciated using the straight line method over a period of 27.5 years, while commercial properties utilize a 39-year period. Another factor affecting straight line depreciation calculations is the salvage value. The salvage value, also known as the residual value, represents the estimated amount an organization can sell the asset for at the end of its useful life.

After you gather these figures, add them up to determine the total purchase price. Now it’s time to calculate the asset’s life span and salvage value. Straight line depreciation is a common method of depreciation where the value of a fixed asset is reduced over its useful life. Depreciation means reducing the value of an do i have to file taxes in multiple states asset for business and tax purposes. Most businesses have assets they need to depreciateStraight-line depreciation is a common method. Things wear out at different rates, which calls for different methods of depreciation, like the double declining balance method, the sum of years method, or the unit-of-production method.

So if the asset was acquired on the first day of the accounting year, the time factor would be 12/12 because it has been available for the entirety of the first accounting year. If an asset is purchased halfway into an accounting year, the time factor will be 6/12 and so on. There are various accounting softwares that help in calculating the same accurately and quickly. However, this process assumes that the fall in value is equal in all years, which may not always be practical.